Introduction to Balance Care Insurance

Let’s cut through the corporate fluff. You are reading this because the American healthcare system is a labyrinth. Balance Care Insurance isn’t just a policy; it’s a tactical maneuver to keep your savings from being swallowed by a hospital’s billing department.

In this deep dive, we’re stripping away the jargon to look at:

- Why Balance Care Insurance is the only metric that matters for your 401(k).

- The Firewall Effect of high limit protection.

- Navigating the gut punch of out of pocket maximums.

- How to leverage the Preventive Dividend to lower your overhead.

- 10 cold, hard answers to the questions your HR department won’t explain.

Healthcare is a Debt Trap Here is the Escape Hatch

The math is brutal. A three day stay in a US hospital for a cardiac event can easily breach the

$60,000 mark Without a specialized shield like Balance Care Insurance, that debt doesn’t just sit there it erodes your life.

What makes the Balanced model different? It’s the actuarial sweet spot. It ignores the noise of low priority claims to ensure that when the Big One hits cancer, major trauma, or chronic illness your financial exposure is capped. It is about buying certainty in an uncertain world.

The protection of Your Personal Wealth

Think of your health as a volatile stock and your insurance as a hedge. When we talk about protecting your lifestyle, we’re talking about Balance Care Insurance as an asset class. It creates a definitive Stop Loss order on your bank account.

By strategically choosing a plan that balances your monthly premium against your potential disaster spend, you aren’t just buying medical access You’re buying the freedom to know that your mortgage and your kids’ tuition are safe, regardless of what a blood test says.

Selecting the Center of Excellence

Not all doctors are created equal. A professional Balance Care Insurance plan doesn’t just give you a directory of names; it gives you a VIP pass to Centers of Excellence. These are surgical units that don’t just do heart surgery they dominate it, with lower infection rates and faster recovery times.

In the balanced model, the quality of the network is the primary feature. You are effectively hiring a team of medical auditors to pre screen your specialists, ensuring you don’t end up in a cut rate clinic during a crisis.

The Digital Handshake: Killing the Paper Trail

We’re in 2026. If you’re still mailing paper claim forms, you’re losing. Modern Balance Care Insurance runs on a Direct Settlement engine. Your digital ID card is a financial passport.

When you check into a network facility, the Digital Handshake happens instantly. The hospital knows the insurer is good for the money, and the insurer knows the hospital is charging a fair market rate. This eliminates the surprise bill that ruins so many American lives.

Cracking the Premium Optimization Code

Most people get the premium to deductible ratio completely wrong. They chase the lowest monthly payment and get blindsided by a $10,000 deductible.

Professional Balance Care Insurance management is about the Total Cost of Ownership. You want to find the equilibrium where your tax advantaged contributions (like an HSA) cover your deductible, while the insurance covers the catastrophic ceiling. It’s a chess match against the insurer, and the Balanced plan gives you the best pieces on the board.

The Care Continuum: From Diagnosis to Physical Therapy

A medical event is a marathon, not a sprint. Balance Care Insurance understands that the surgery is just the middle point. The real costs hide in the 60 days of diagnostic testing before the operation and the 90 days of rehabilitation after you’re discharged.

A high end policy covers the entire timeline. It ensures that the MRI that found the problem and the physical therapist who gets you walking again are all part of the same financial umbrella.

The Outpatient Revolution: Why Daycare is the Future

Medical tech has moved faster than the law. We now have robotic surgeries that allow you to go home the same afternoon. In the past, insurance wouldn’t pay if you weren’t admitted.

Balance Care Insurance has fixed this glitch. It covers Daycare Procedures complex medical interventions that happen in a few hours. Whether it’s a specialized eye surgery or an orthopedic repair, the Balanced model focuses on the procedure’s complexity, not the bed’s occupancy.

The Wellness Dividend: Getting Paid to Stay Fit

In the most honest version of healthcare, the insurer wins when you don’t get sick. Balance Care Insurance leans into this by offering Wellness Rewards.

We’re talking about premium credits for non smokers, discounts for hitting step goals tracked via your Apple Watch, and zero cost annual metabolic panels. It’s the ultimate incentive: live a better life, pay a lower bill. It’s the Balanced lifestyle in its truest form.

Mental Health: The Invisible Front Line

The stigma is gone, but the costs remain. Modern Balance Care Insurance has elevated behavioral health to a primary benefit. This includes tele therapy for burnout, psychiatric support for depression, and inpatient care for severe episodes. By treating the mind with the same urgency as a broken leg, these policies prevent the long term physical decline that often follows mental health struggles.

Maternity Stewardship: Protecting the Next Generation

In the US, a normal delivery is expensive, and a complicated one is astronomical. Balance Care Insurance provides a Maternity Stewardship framework. This isn’t just about the birth; it’s about the prenatal genetic screenings and the neonatal intensive care (NICU) safety net. It allows parents to focus on the child, while the policy handles the high stakes billing.

Radical Transparency: The No Go Zone

A professional guide has to be honest: insurance doesn’t cover everything. Balance Care Insurance is a medical tool, not a lifestyle fund.

It won’t pay for your nose job (unless it’s reconstructive), it won’t pay for experimental fountain of youth drugs, and it won’t pay for injuries sustained while you were BASE jumping without a rider. Knowing these boundaries is what prevents your claim from getting rejected when you need it most.

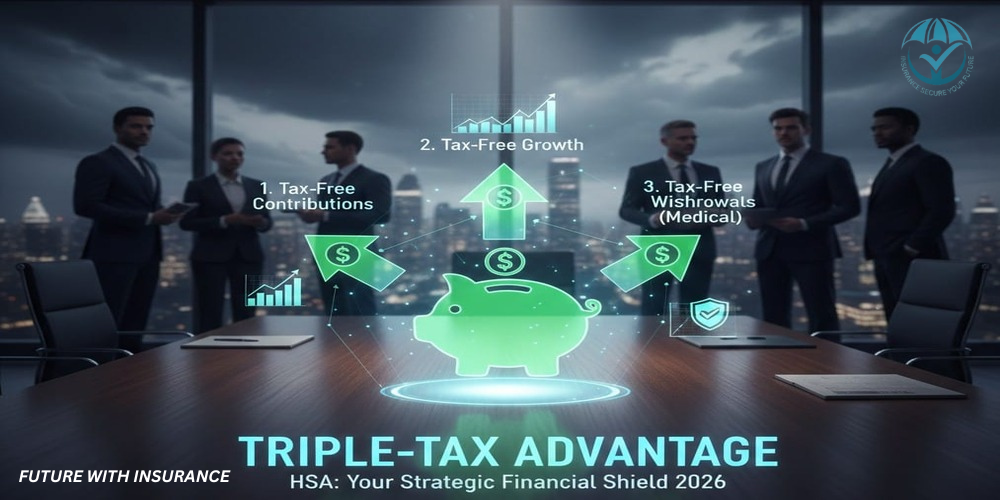

The HSA Synergy: Your Secret Tax Weapon

If your Balance Care Insurance is HSA compatible, you’ve hit the tax jackpot. This is a Triple Tax Advantage

- The money goes in before taxes.

- It grows tax free.

- You spend it tax free on medical bills.

It effectively gives you a 25% discount on your entire healthcare spend. It is the single most powerful financial move a policyholder can make.

Strategic Claim Mastery: Don’t Be a Victim

Filing a claim shouldn’t be a gamble. Follow the Rule of Three:

- The Double Check: Confirm the doctor, not just the building, is in network.

- The Pre Auth: For any surgery, get the digital authorization code 72 hours early.

- The Audit: Read your Explanation of Benefits like a private investigator. Hospitals make mistakes; your job is to catch them.

The Family Floater Power Play

For anyone with kids, the Individual Plan is a mistake. The Family Floater is the winner. It treats your family as one unit with one giant pool of coverage. Since it’s rare for everyone to get sick at once, the Floater gives you a much higher coverage ceiling for every dollar of premium you pay. It’s basic probability working in your favor.

Conclusion: The Ultimate Asset

In the end, Balance Care Insurance is about buying back your peace of mind. It’s the quiet confidence that no matter what happens in the lab or on the operating table, your family’s future is ironclad. It is an investment in the one thing that truly matters: the time you have left, free from financial fear.

Top 10 Hard Hitting FAQs

1. Is Balance Care Insurance just a fancy name for a PPO?

Not exactly. While it shares the flexibility of a PPO, it is usually more tech forward, with built in restoration benefits and aggressive wellness incentives that traditional PPOs lack.

2. What the heck is Sum Insured Restoration?

It’s a reset button. If you use your $100k limit on one illness, the policy refills for the next unrelated illness in the same year. It’s a life saver.

3. Will my premium skyrocket if I get cancer?

No. Under US law, an insurer cannot raise your individual rate just because your health declines. They can only raise rates for the entire risk pool in your area.

4. Does it cover my meds?

Yes, but look at the Formulary. Generic drugs are usually $10, while Tier 4 specialty drugs might require a larger co pay or prior authorization.

5. I travel a lot for work. Am I covered?

Domestic travel? Yes. International? Usually only for Emergency Only unless you add a specific global rider to your plan.

6. What if I want a second opinion from the Mayo Clinic?

Most balanced plans actually pay for this. They want you to have the right diagnosis because a wrong one costs them more in the long run.

7. Can I keep my policy if I’m fired?

If it’s a private plan, yes. If it was employer based, you’ll have to use COBRA (which is expensive) or switch to an individual balanced plan.

8. Are Alternative treatments like Acupuncture covered?

Increasingly, yes but usually with a cap on the number of sessions per year and a requirement that it’s for pain management.

9. How fast is a Cashless approval?

Usually 2 to 4 hours. For an emergency, the hospital will stabilize you first and handle the paperwork once you’re in a room.

10. What is an HSA and why should I care?

It’s a Health Savings Account. It’s the only way to pay for your deductible using tax free money. If you have a balanced plan, you need an HSA.